World Technology Congress, Thursday, 23 April 2026, Lake Como, Italy

Distinguished guests, ladies and gentlemen,

The Ethics Manual We Never Wrote

I want to begin with a confession. I came to Lake Como this week telling myself it was a professional duty. But with this weather and this location, I have since revised that position. The view is magnificent, but the problem we’re here to discuss is also extraordinary: we have built the most powerful cognitive tools in human history, and we shipped them without an ethics manual.

Thrive in Life Sciences The London Centre, Guildhall 10.15, Monday 21st October 2024 The Rt Hon The Lord Mayor of London, Alderman Professor Michael Mainelli

Good morning, everyone.

As leader of the City of London Corporation – what I affectionately like to refer to as the world’s oldest democratic workers’ and residents’ cooperative – let me say how wonderful it is to have you all here today in the heart of the Square Mile.

The City of London has always been a hub of learning, creativity, and science. Indeed, it is almost 360 years to the day that the City’s great chronicler, Samuel Pepys, wrote in his diary upon being admitted to the Royal Society:

“It is a most acceptable thing to hear their discourse and see their experiments; which were this day upon the nature of fire, and how it goes out in a place where the ayre is not free, and sooner out where the ayre is exhausted, which they showed by an engine on purpose.”

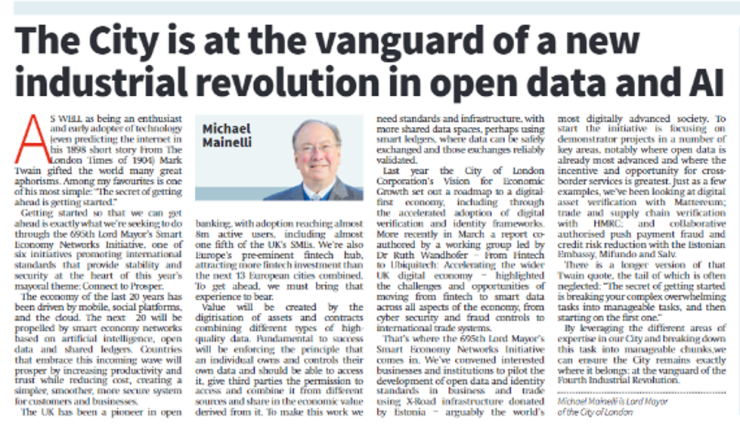

The discourses we have heard this morning are a continuation of that proud legacy we have across London, one that sees 40 learned societies, 70 higher education institutions, and 130 research institutes located within a mile and a half of where we gather today. When the Royal Society was founded in 1660 it was done so by scientists – or natural philosophers as they were called back then – but also by people who made their living as architects, astronomers, mathematicians, clergymen, and even spies.

Why? Because they recognised that the life sciences only thrive when they work on a multidisciplinary basis – a principle that remains true today. Want an example?

Some of you may have heard about the connectome – an incredibly accurate 3D map – that was recently completed of a fruit fly’s brain. You could say that there’s been a bit of buzz around the news.

Supporting Dr Mala Murthy and Dr Sebastian Seung of Princeton University – the neuroscientists that made the breakthrough – were 622 researchers specialising in different fields from 146 laboratories around the world …not to mention computer scientists, engineers, financiers, and 15 enthusiastic “citizen scientist” video-gamers who helped proofread and annotate the results.

By identifying and mapping the different types of neurons in the fly’s brain, the research will not only help us better understand our own neurological workings – for example how our brains respond to different stimuli like lights, sounds, and smells – but could also support the development of the AI models that made the creation of the connectome possible in the first place.

That potential to make headway on the intractable challenges we face is the reason why promoting multidisciplinary networks sits at the heart of this year’s mayoral theme – Connect to Prosper – through which we’re celebrating the City’s many different areas of expertise – the Knowledge Miles of the Square Mile – showcasing London as the world’s coffee house, a place where people come together, from across the globe, to find solutions to our planet’s biggest problems, from mental health to climate change.

On top of experiments, lectures, and expert networking sessions, as part of Connect to Prosper we’ve launched six exciting initiatives all promoting practical solutions:

The Ethical AI Initiative, using ISO standards.

The Space Protection Initiative, using space debris removal insurance bonds.

The Smart Economy Networks Initiative, using international X-Road standards.

The Green Finance Initiative, reinforcing carbon markets. And two that may be of particular interest today:

GALENOS, accelerating global mental health research through a state-of-the art online resource which pulls together the best early-phase science into a continuously updated and trustworthy catalogue, allowing the mental health community to better identify the research questions that most urgently need to be answered.

And our Constructing Science Initiative, through which we’re highlighting the potential for life science and other laboratories around London and providing an international standard for those seeking to convert vacant offices to life science facilities.

None of this would be possible without connections – intra and inter sectoral, both here in the UK and abroad. The connections being made this morning through this coalition led by 8 local authorities and MedCity are of real value, with the skills and expertise everyone here brings contributing to its important mission to create a diverse life sciences ecosystem.

It has been especially pleasing to see the progress that has been made on developing inclusive career pathways since we last met in May, but scaling the sort of initiatives and pilots we have heard about will require further resource – a challenge all of us need to find solutions to together.

Henry Ford once said: “Coming together is a beginning; keeping together is progress; working together is success.” And over the coming weeks and months we must keep working together if we are to make good on the ambitions of the coalition.

My sincere thanks to everyone who has contributed to this morning’s informative discussions. But especially to Paul Singh, our Connect to Prosper Life Sciences Lead, for all the work he is doing, and of course to Central London Forward, Lateral, and H.I.G. Capital who have sponsored this morning’s breakfast and the forthcoming careers event for primary school children being held on 7th November.

We still have this room for the next half an hour or so, so please stay, network, and continue to connect to prosper. Thank you.

Lord Mayors get to choose a charity for the Lord Mayor’s Appeal. The chosen charity is supported on a ‘transformational project’ for three years; thus three are being supported at any one time. The Lord Mayor’s Appeal helps deserving causes across the capital and is generously supported by the City of London’s livery companies. The generosity of freemen and the livery companies, along with support from City A.M. and businesses for events like City Giving Day, provide the funding.

My choice for the Lord Mayor’s Appeal was the charity MQ Mental Health Research as one of our three chosen partner organisations. MQ’s founding supporter, the Wellcome Trust – based in London – is one of the world’s largest global health science foundations. Together, we approached mental health by putting science at its heart.